The most crucial component of an automobile-financial loan is arguably the curiosity level. It instantly influences the size of regular monthly payments and total loan tenor. Fascination costs can even perform a position in the remaining shopping for decision, effective more than enough to override sentimental invest in factors these as manufacturer loyalty. It goes without saying, therefore, that opportunity vehicle purchasers fork out focus to elements that decide their fascination premiums when searching for automobile-financing alternatives.

1 of this sort of variables is the credit rating rating. It is essentially a weighted score that tells vehicle-creditors how a lot chance they are taking on by dealing with a future borrower. You most possible have a credit report if you have any credit accounts, these kinds of as credit score playing cards, mortgages or loans. This report then sorts the foundation for pinpointing your credit history score.

It is not an specific evaluate, but it does get rid of mild on elements this kind of as the borrower’s willingness and capacity to company the personal loan. Simply put, the better your credit history score, the greater your likelihood of securing an car financial loan with favourable interest charges. This is specifically vital today as we navigate the period of desire fee hikes and inflationary pressures.

Applying your credit score score to safe the most effective desire costs

Through Experian

The over-all purpose of the credit rating rating is universal. Having said that, different creditors in distinct elements of the environment have their individual conditions to evaluate an individual’s creditworthiness. When you utilize for an auto bank loan in the US, the loan provider will operate a credit look at as element of the process. The majority of the lending institutions use FICO credit rating scores. This is a 3-digit score assigned to a borrower just after the credit test work out.

It was to begin with developed in 1989 by a data analytics firm termed Honest Isaac Business. Now, there are lots of variations of the FICO algorithm (and other scoring types, for that issue), but they are all aimed at ascertaining the borrower’s potential to just take on credit history.

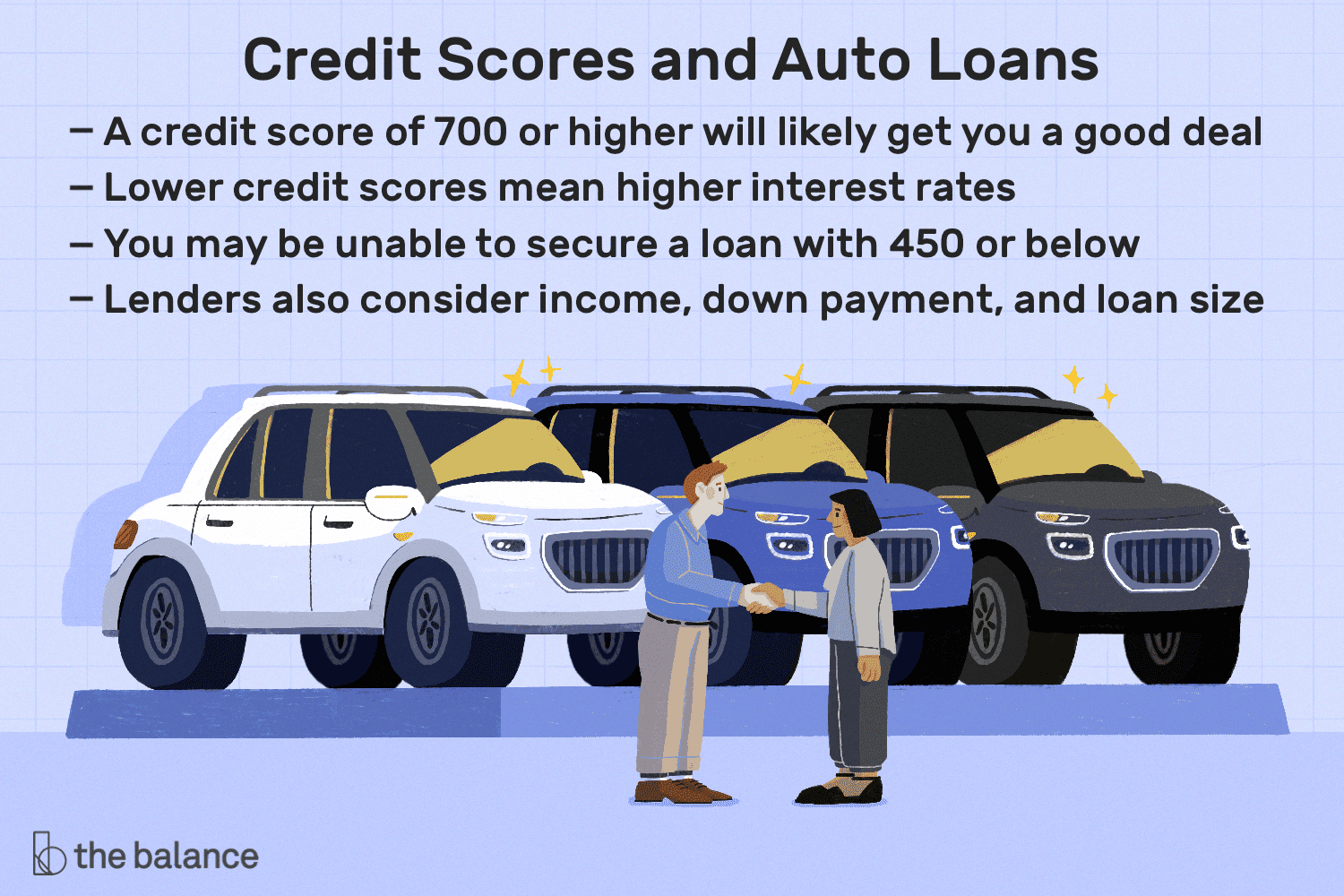

By way of The Balance

According to the CFPB (Consumer Fiscal Protection Bureau) Consumer Credit history Panel, there are 5 different borrower profiles sorted into the subsequent credit history rating buckets: Super-prime (720 & over) Key (660-719) Close to-key (620-659) Subprime (580-619) Deep subprime (under 580). A borrower with a rating under 660 can however protected car financial loans, but they will be much more pricey than a Primary or Tremendous-prime borrower with a rating north of 661. The logic here is that you will want to keep your credit rating rating as high as feasible to get the finest offers when browsing for car financial loans.

Points that hurt your credit score score

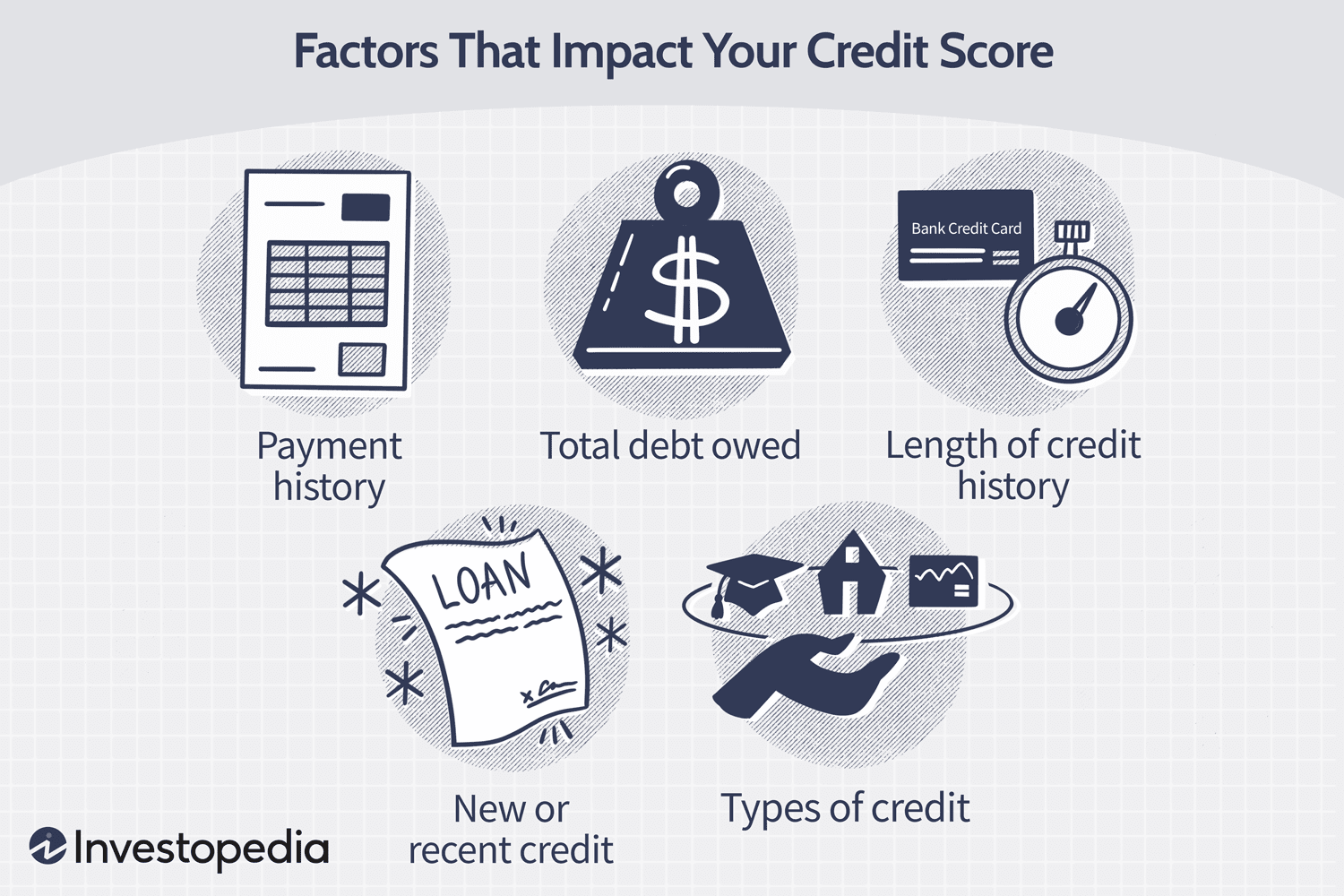

By using Investopedia

An excellent credit score is the end result of watchful and deliberate scheduling, and recognizing the probable pitfalls can support the borrower keep away from building missteps that pull down the score into unwanted territory.

Creating a late payment

Payment history on your credit obligations accounts for up to 35% of the FICO score. According to FICO, a payment that is 30 days late can value an individual with a credit rating of 780 or greater any place from 90 to 110 details. It is crucial to make payments as at when because of and proactively get to out to the loan provider if, for any reason, payment will be delayed.

A substantial personal debt-to-credit history utilization ratio

Credit rating historical past is crafted by a continual cycle of credit history utilization and spend downs. Nevertheless, you will want to maintain an eye on the proportion of your debt load to all round credit rating. The decreased your balances relative to your full readily available credit score, the superior your score will be.

Non-utilization of credit

On the other hand, no credit rating history for an extended interval can also adversely affect the borrower’s credit history score. Lenders and lenders have almost nothing to report to credit history bureaus when you don’t make use of your credit score accounts. This makes it a lot more challenging to examine potential personal loan programs.

Personal bankruptcy

Filing for bankruptcy has a single of the most considerable impacts on your credit score score. It can wipe as a great deal as 240 details from an individual’s score, and what is far more? A personal bankruptcy report can keep on the credit score heritage for up to ten several years.

This listing is by no indicates exhaustive, and other variables these types of as frequency of credit programs, credit card closure, demand-offs and refinancing all impression credit rating scores in different degrees.

Enhancing your credit history score

Increasing your credit rating score will contain preventing the pitfalls previously discovered over. Procedures these kinds of as prompt and regular monthly bill payments, keeping a reduced credit card debt-to-credit history utilization ratio (preferably about 30%), retaining credit history card accounts open up and staying away from quite a few bank loan purposes at when are all actions in the suitable route.

Nevertheless, even with all these ‘building blocks’ in put, a fantastic credit history score is not instantaneous. It may well choose a even though to see any improvement, especially because unfavorable experiences can continue to be on your credit score background for a number of years. There is no rigid time frame for credit history rating advancement as every person’s monetary condition is distinctive. In accordance to Forbes, it could get everywhere from a thirty day period to as much as ten a long time. Naturally, this is influenced by elements such as the individual’s present-day credit history standing and amount of money of full publicity.

Securing auto loans irrespective of credit rating rating

Through Geotab

A superior credit rating score will certainly boost your possibilities of securing vehicle funding and locking up the greatest fascination charges. However, it is not all doom-and-gloom for possible motor vehicle consumers with weak scores as they are not solely without the need of choices.

Irrespective of your credit rating, wanting around and taking into consideration the numerous funding choices is remarkably advisable. It is just like browsing for the car itself an ordinary customer will assess diverse dealerships and negotiate vigorously in advance of building the last decision.

Financial institutions are the classic resources for acquiring a personal loan, but you might be limiting your possibilities if they are your only thought. Never ignore alternative loan providers. Functioning with third-social gathering financing companies, such as getting your automobile financial loan through LoanCenter.com, may perhaps provide you with favourable interest prices or funding terms.

It is important to observe that simply acquiring auto-bank loan preapprovals (various from actual bank loan apps) even though buying about will not affect your credit score rating since most scoring types do not deal with this as a really hard enquiry.

In summary, a weak credit score score could force the most affordable interest charges out of attain. However, acquiring numerous alternatives will boost your possibilities of obtaining a package deal with an curiosity fee that suits inside your spending plan and allow for you to obtain your ideal auto.

More Stories

Study: We All Think Distracted Driving Is a Problem. Many Do It Anyway.

Genesis X Convertible Concept – Car Body Design

This is How You Build a BMW M2 Competition for the Road and Track